{kind=link}

Key Takeaways

- Poor communications are driving buyer churn, with one in 4 shoppers aged 18–43 switching suppliers after a foul expertise.

- Clear knowledge is desk stakes, not a differentiator; what creates a superior buyer expertise is built-in, contextually utilized knowledge that powers personalised, real-time communications.

- To modernize buyer communications, monetary establishments want a modular strategy throughout expertise, knowledge, and other people.

When talking with our monetary companies clients, we’re noticing some remarkably constant challenges: fragmented programs, unrealized returns on digital investments, mounting AI complexity, and the ever-present strain to keep up buyer belief.

These widespread challenges usually really feel like we’re all singing the identical tune, simply with barely totally different lyrics.

Nevertheless, there was a shift lately and that urgency. Prospects are performed being affected person. And for banks nonetheless working with document-centric, one-way communications, that impatience is exhibiting up straight in churn numbers — making buyer expertise modernization much less of a roadmap merchandise and extra of a aggressive crucial.

Why Poor Financial institution Communications Are Driving Buyer Churn

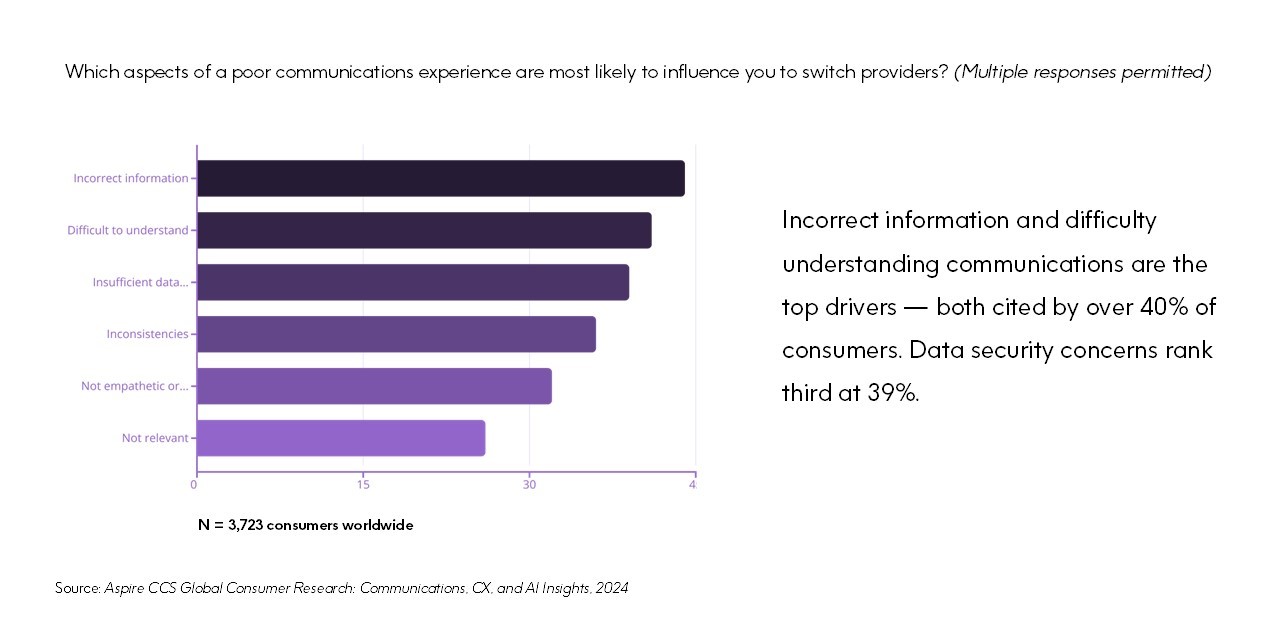

Based on analysis from Aspire, one in 5 shoppers have switched suppliers prior to now 12 months attributable to a poor communications expertise. Amongst shoppers aged 18–43, that quantity jumps to 1 in 4. It’s clear that youthful, extra prosperous, and tech-savvy shoppers aren’t going to attend so that you can determine your communications challenges.

And once you take a look at why they’re switching, it’s not about charges or charges. 5 of the highest six causes come again to the communications themselves: incorrect info, content material that’s arduous to know, inconsistencies throughout channels, messaging that doesn’t really feel related.

I take into consideration this personally. My dad and I each had the identical insurer. I had a horrible expertise — complicated billing, poor communication, zero personalization — and I left. He stayed, although he complains in regards to the cost course of each single quarter. His expectations of brand name expertise are decrease, and he’s prepared to tolerate communication missteps.

That’s high-quality, but it surely illustrates one thing necessary: when you’re making an attempt to develop and retain clients, tolerance isn’t the identical as loyalty.

Why Are Distinctive Banking Experiences So Laborious? 4 Challenges We’re All Navigating

After we speak to banking and monetary companies organizations, 4 themes repeatedly come up.

- Unrealized returns. We’ve been speaking about digital transformation for years, and but a lot of these investments haven’t delivered. Experiences nonetheless fail to contextualize a buyer’s precise state of affairs or information them towards a logical subsequent step. We’ve purchased loads of issues, they’re simply not working collectively.

- System fragmentation. That tech stack drawback is actual. Siloed knowledge, legacy programs, and disconnected groups imply that even when the proper knowledge exists someplace, it’s not flowing the place it must go to energy higher communications. An viewers ballot throughout our latest webinar with American Banker confirmed what we see always within the area: 53% of respondents cited organizational silos and lack of cross-functional alignment as their greatest barrier to bettering buyer communication — the runaway reply, effectively forward of legacy programs, knowledge high quality, or regulatory constraints.

- AI threat. AI is genuinely serving to groups work quicker and smarter. However constructing with AI with out the precise governance foundations is asking for hassle, together with hallucinations, bias, compliance failures, or just “rubbish in, rubbish out.” At the same time as AI brokers change into extra succesful, the necessity for human approval loops and lifecycle controls has solely grown.

- Buyer belief. Even with personalization capabilities in place, organizations are sometimes restricted in how far they’ll take it. Prospects are more and more conscious of how their knowledge is getting used, and any interplay that feels invasive or “creepy” can erode belief rapidly. Getting hyper-personalization proper means incomes that belief transparently, not simply technically.

Why Clear Knowledge Isn’t Sufficient for Your Buyer Communications

You may have an handle that’s spelled accurately. You may have account numbers that match. You may have technically correct knowledge throughout your programs … and nonetheless ship a communication that feels chilly, irrelevant, or complicated.

Knowledge high quality is desk stakes. What creates a compelling buyer expertise is knowledge that’s built-in, contextually related, and utilized intelligently in the intervening time of communication.

Give it some thought this manner: a buyer may need a mortgage, a checking account, and a bank card with the identical financial institution. But when these three product traces reside in separate programs (which they usually do), the communications popping out of every can really feel like they’re from three totally different corporations.

Worse, you’ll be able to find yourself in conditions the place a collections discover for a missed cost goes out on the identical day as a “you’re a valued buyer” promotional provide.

Most of us have doubtless been on the receiving finish of those mishaps. And the actual challenge isn’t that the info was mistaken, however that the context was lacking.

Aspire’s 2025 enterprise analysis discovered that three quarters of companies worldwide imagine AI will basically rework the best way they convey with clients. Six in ten have already applied AI into their communications at some stage.

WEBINARFrom Paperwork to Dialogue: Modernizing financial institution communications with trusted knowledge and AI

On this session, you’ll find out how a contemporary, cloud-native and ruled communications platform permits banks to enhance readability, keep compliance, speed up workflows, and ship personalised, constant engagement throughout each channel.

How one can Modernize Monetary Providers CCM: Three Areas to Deal with

There’s no single lever to tug right here. Actual modernization-powered transformation — transferring from static, one-way paperwork to personalised, two-way dialogue — requires progress throughout three interconnected areas.

- Trendy omnichannel platforms must do greater than help digital channels. They should help AI-assisted workflows, combine with the broader tech stack, and function inside a safe, cloud-native surroundings. A important piece that usually will get missed: as organizations construct out AI brokers throughout departments, you want a shared semantic layer — basically a information graph — to assist these brokers talk meaningfully with one another and keep away from creating new silos beneath the hood.

- Trusted, decision-ready knowledge requires deliberate funding in knowledge merchandise, governance throughout threat, fraud, underwriting, and servicing capabilities, and embedded intelligence that may allow real-time decisioning on the level of buyer motion. The extra proactive you may be with that intelligence, the higher the expertise and the stronger the model loyalty.

- Organizational alignment. Ballot after ballot, dialog after dialog, that is the one. Getting communications proper in monetary companies goes far past simply expertise. It requires enterprise traces, IT, compliance, and customer-facing groups to cease working in their very own silos. Meaning having conversations together with your Chief Knowledge Officer, your Chief Compliance Officer, your playing cards staff, and extra. — Constructing a cross-functional governance mannequin that treats communications as a shared duty is important.

One other ballot in our American Banker webinar strengthened simply how early most organizations nonetheless are on this course of: 44% stated they’re actively modernizing however solely partway via, and one other 33% are nonetheless evaluating trendy platforms. That’s almost 80% of respondents mid-journey or earlier — which implies the window to construct an actual aggressive benefit via communications continues to be broad open.

Your Legacy CCM?

Quick reply: in all probability not.

The extra sincere reply: it is dependent upon what you’re working with. When you have a homegrown answer that somebody stitched collectively 30 years in the past, has no documentation, and the architect retired — and also you’re now making an attempt to layer AI on prime of it — then sure, that’s an issue that finally must be solved. However for many organizations, the trail ahead isn’t a big-bang substitute.

What works higher is a modular strategy: establish the place the ache is most acute, the place the governance threat is highest, the place a regulatory change that ought to take a day continues to be taking 90. Begin there. Migrate these high-stakes communications first, set up your ruled platform, construct the info basis — after which increase.

And critically: be certain that the technique is evident earlier than the funding is made. Deploying AI for AI’s sake, or shopping for expertise with no outlined drawback to unravel, hardly ever ends effectively.

Make the Shift from Doc-Centric to Dialogue-Pushed Communications

The imaginative and prescient is a buyer communications expertise that appears like a pure, personalised dialog.

One the place a mortgage buyer will get a personalised, participating video abstract of their mortgage phrases earlier than they arrive in to signal, quite than sitting via an hours-long, in-person walkthrough. One the place a collections discover displays what’s really occurring in a buyer’s life. One the place a banking app proactively surfaces the precise info on the proper second, quite than sending the identical generic app-download immediate to somebody who’s been utilizing the app for a decade.

That form of expertise requires the precise knowledge basis, governance mannequin, and communications platform. EngageOne RapidCX from Exactly is constructed for precisely this — serving to monetary establishments transfer from fragmented, document-centric CCM to ruled, AI-assisted, omnichannel engagement, designed to work throughout the compliance and regulatory necessities that make monetary companies uniquely advanced.

RapidCX from Exactly is constructed for precisely this — serving to monetary establishments transfer from fragmented, document-centric CCM to ruled, AI-assisted, omnichannel engagement, designed to work throughout the compliance and regulatory necessities that make monetary companies uniquely advanced.

However greater than any single product, what issues is a strategic strategy: know the issue you’re fixing, construct on trusted knowledge, align your group — after which put money into expertise that strikes you ahead. Study extra:

- Watch our on-demand webinar: From Paperwork to Dialogue: Modernizing financial institution communications with trusted knowledge and AI.

- And get your copy of the Aspire report: Constructing Dialogue – Pushed Engagement

The put up Financial institution CCM Modernization: From Paperwork to Dialogue with AI appeared first on Exactly.