{kind=link}

10 Python One-Liners for Producing Time Collection Options

Introduction

Time collection information usually requires an in-depth understanding with a view to construct efficient and insightful forecasting fashions. Two key properties are important in time collection forecasting: illustration and granularity.

- Illustration entails utilizing significant approaches to rework uncooked temporal information — e.g. each day or hourly measurements — into informative patterns

- Granularity is about analyzing how exactly such patterns seize variations throughout time.

As two sides of the identical coin, their distinction is delicate, however one factor is definite: each are achieved by way of characteristic engineering.

This text presents 10 easy Python one-liners for producing time collection options primarily based on completely different traits and properties underlying uncooked time collection information. These one-liners can be utilized in isolation or together that will help you create extra informative datasets that reveal a lot about your information’s temporal conduct — the way it evolves, the way it fluctuates, and which traits it displays over time.

Observe that our examples make use of Pandas and NumPy.

1. Lag Function (Autoregressive Illustration)

The concept behind utilizing autoregressive illustration or lag options is less complicated than it sounds: it consists of including the earlier statement as a brand new predictor characteristic within the present statement. In essence, that is arguably the best technique to symbolize temporal dependency, e.g. between the present time instantaneous and former ones.

As the primary one-liner instance code on this listing of 10, let’s have a look at this yet one more carefully.

This instance one-liner assumes you could have saved a uncooked time collection dataset in a DataFrame referred to as df, one in all whose current attributes is called 'worth'. Observe that the argument within the shift() perform may be adjusted to fetch the worth registered n time instants or observations earlier than the present one:

|

df[‘lag_1’] = df[‘value’].shift(1) |

For each day time collection information, for those who wished to seize earlier values for a given day of the week, e.g. Monday, it might make sense to make use of shift(7).

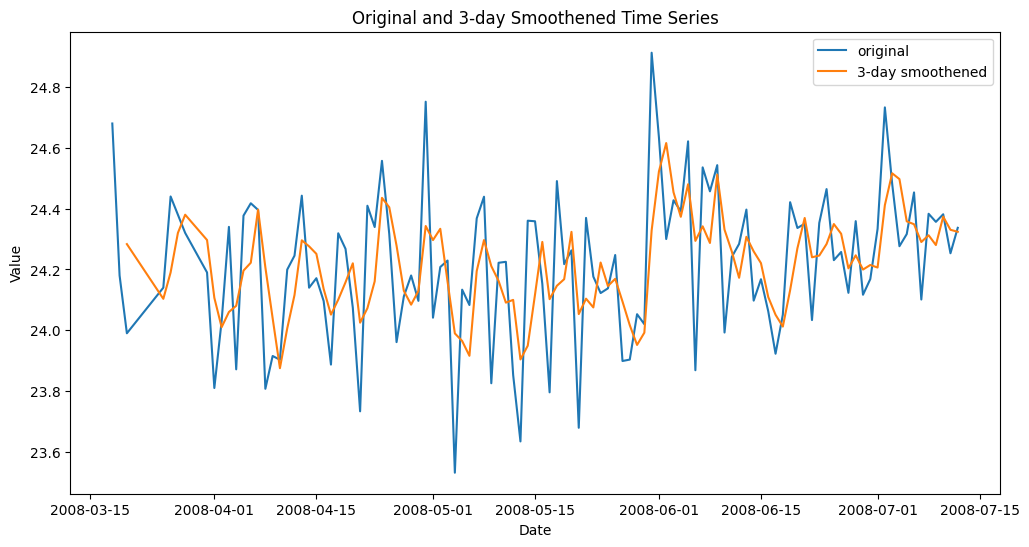

2. Rolling Imply (Brief-Time period Smoothing)

To seize native traits or smoother short-term fluctuations within the information, it’s often useful to make use of rolling means throughout the n previous observations resulting in the present one: it is a easy however very helpful solution to clean generally chaotic uncooked time collection values over a given characteristic.

This instance creates a brand new characteristic containing, for every statement, the rolling imply of the three earlier values of this characteristic in current observations:

|

df[‘rolling_mean_3’] = df[‘value’].rolling(3).imply() |

Smoothed time collection characteristic with rolling imply

3. Rolling Commonplace Deviation (Native Volatility)

Just like rolling means, there’s additionally the potential of creating new options primarily based on rolling commonplace deviation, which is efficient for modeling how unstable consecutive observations are.

This instance introduces a characteristic to mannequin the variability of the newest values over a shifting window of every week, assuming each day observations.

|

df[‘rolling_std_7’] = df[‘value’].rolling(7).std() |

4. Increasing Imply (Cumulative Reminiscence)

The increasing imply calculates the imply of all information factors as much as (and together with) the present statement within the temporal sequence. Therefore, it is sort of a rolling imply with a always rising window dimension. It’s helpful to research how the imply of values in a time collection attribute evolves over time, thereby capturing upward or downward traits extra reliably in the long run.

|

df[‘expanding_mean’] = df[‘value’].increasing().imply() |

5. Differencing (Development Elimination)

This method is used to take away long-term traits, highlighting change charges — essential in non-stationary time collection to stabilize them. It calculates the distinction between consecutive observations (present and former) of a goal attribute:

|

df[‘diff_1’] = df[‘value’].diff() |

6. Time-Based mostly Options (Temporal Element Extraction)

Easy however very helpful in real-world functions, this one-liner can be utilized to decompose and extract related data from the total date-time characteristic or index your time collection revolves round:

|

df[‘month’], df[‘dayofweek’] = df[‘Date’].dt.month, df[‘Date’].dt.dayofweek |

Necessary: Watch out and test whether or not in your time collection the date-time data is contained in a daily attribute or because the index of the info construction. If it have been the index, you might want to make use of this as an alternative:

|

df[‘hour’], df[‘dayofweek’] = df.index.hour, df.index.dayofweek |

7. Rolling Correlation (Temporal Relationship)

This strategy takes a step past rolling statistics over a time window to measure how current values correlate with their lagged counterparts, thereby serving to uncover evolving autocorrelation. That is helpful, for instance, in detecting regime shifts, i.e. abrupt and chronic behavioral adjustments within the information over time, which occur when rolling correlations begin to weaken or reverse sooner or later.

|

df[‘rolling_corr’] = df[‘value’].rolling(30).corr(df[‘value’].shift(1)) |

8. Fourier Options (Seasonality)

Sinusoidal Fourier transformations can be utilized in uncooked time collection attributes to seize cyclic or seasonal patterns. For instance, making use of the sine (or cosine) perform transforms cyclical day-of-year data underlying date-time options into steady options helpful for studying and modeling yearly patterns.

|

df[‘fourier_sin’] = np.sin(2 * np.pi * df[‘Date’].dt.dayofyear / 365) df[‘fourier_cos’] = np.cos(2 * np.pi * df[‘Date’].dt.dayofyear / 365) |

Enable me to make use of a two-liner, as an alternative of a one-liner on this instance, for a cause: each sine and cosine collectively are higher at capturing the massive image of doable cyclic seasonality patterns.

9. Exponentially Weighted Imply (Adaptive Smoothing)

The exponentially weighted imply — or EWM for brief — is utilized to acquire exponentially decaying weights that give increased significance to current information observations whereas nonetheless retaining long-term reminiscence. It’s a extra adaptive and considerably “smarter” strategy that prioritizes current observations over the distant previous.

|

df[‘ewm_mean’] = df[‘value’].ewm(span=5).imply() |

10. Rolling Entropy (Info Complexity)

A bit extra math for the final one! The rolling entropy of a given characteristic over a time window calculates how random or unfold out the values over that point window are, thereby revealing the amount and complexity of knowledge in it. Decrease values of the ensuing rolling entropy point out a way of order and predictability, whereas the upper these values are, the extra the “chaos and uncertainty.”

|

df[‘rolling_entropy’] = df[‘value’].rolling(10).apply(lambda x: –np.sum((p:=np.histogram(x, bins=5)[0]/len(x))*np.log(p+1e–9))) |

Wrapping Up

On this article, we’ve examined and illustrated 10 methods — spanning a single line of code every — to extract quite a lot of patterns and data from uncooked time collection information, from easier traits to extra refined ones like seasonality and data complexity.